INTRODUCTION

Earnings announcements and exogenous events may be unpredictable but the ways investors react to them are not. At times, no matter how much negative news, the proverbial glass still seems half full and sometimes no amount of good news can change the investors’ view of the glass as half empty.

Mood sentiments are well known to greatly influence asset prices, at times completely ignoring fundamental valuations, and have been given many names; Ben Graham and later his most famous disciple Warren Buffett labeled it the mano-depressive Mr. Market, J.M. Keynes referred to animal spirits and former Fed chairman Alan Greenspan talked about irrational exuberances (as per quotations below).

As conventional economics has proven ill-equipped to incorporate and account for this seemingly irrational investor behavior, it has in practice rendered the commonly accepted economic and financial theories void. Economists are at loss on how to adapt their theories to adjust for collective human behavior that does not follow the ‘rational man’ assumptions and no one has so far been able to pinpoint these forces and explain its mechanics, other than in an anecdotal fashion. This has led to a greater interest in alternative approaches to economic theory. However applying newer approaches such as behavioral finance has at best proven uneven in predicting and explaining financial bubbles. They all fail to answer the two most important questions Why? and When?

Given the huge impact these fluctuations have on asset prices and the fact that fundamental valuation models does not factor them in at all, it is important to try to understand what the underlying drivers are. So if existing theoretical frameworks seem not able to provide explanatory models, is there another way? Yes, but we have to dwell into depth psychology and explore the mechanics of the collective unconscious and its archetypes before attempting to establish a forecasting methodology.

Quotations

Ben Graham – The Intelligent Investor

Even though the business that the two of you own may have economic characteristics that are stable, Mr. Market’s quotations will be anything but. For, sad to say, the poor fellow has incurable emotional problems. At times he feels euphoric and can see only the favorable factors affecting the business. When in that mood, he names a very high buy-sell price because he fears that you will snap up his interest and rob him of imminent gains. At other times he is depressed and can see nothing but trouble ahead for both the business and the world. On these occasions he will name a very low price, since he is terrified that you will unload your interest on him.

John Maynard Keynes – The General Theory of Employment, Interest and Money

Even apart from the instability due to speculation, there is the instability due to the characteristic of human nature that a large proportion of our positive activities depend on spontaneous optimism rather than mathematical expectations, whether moral or hedonistic or economic. Most, probably, of our decisions to do something positive, the full consequences of which will be drawn out over many days to come, can only be taken as the result of animal spirits – a spontaneous urge to action rather than inaction, and not as the outcome of a weighted average of quantitative benefits multiplied by quantitative probabilities.

Alan Greenspan – “The Challenge of Central Banking in a Democratic Society”, 1996-12-05

[...] Clearly, sustained low inflation implies less uncertainty about the future, and lower risk premiums imply higher prices of stocks and other earning assets. We can see that in the inverse relationship exhibited by price/earnings ratios and the rate of inflation in the past. But how do we know when irrational exuberance has unduly escalated asset values, which then become subject to unexpected and prolonged contractions as they have in Japan over the past decade? [...]

THE COLLECTIVE UNCONSCIOUS

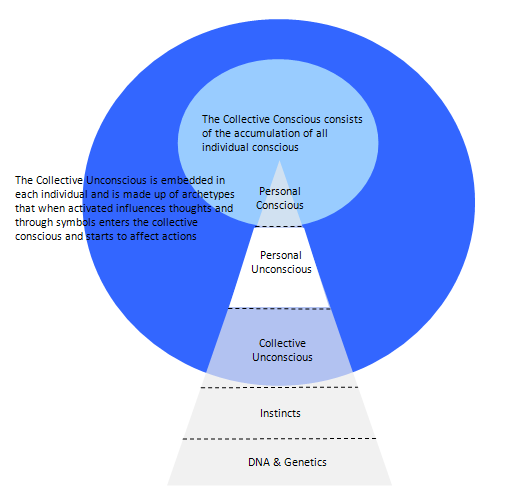

Human choices, both in aggregation and individually, such as investment decisions are affected to a large degree by the prevailing social mood or zeitgeist. It is generally accepted that the collective unconscious plays an important part in determining the contents and directions of these social mood swings. The concept of the collective unconscious evolved and advanced greatly under Carl Gustaf Jung (1875-1961), a Swiss psychologist and initially a disciple of Sigmund Freud, however his differing views on the collective unconscious, among other, led him to later on break with Freud. Jung can thus be seen as one of the founding fathers of the concept on the collective unconscious and its associated archetypes and his views have won broad acceptance among the psychology profession and academics.

Jung defined the collective unconscious as a part of the mind which is not available to consciousness, and he made a clear distinction between the collective unconscious and the personal unconscious. The personal unconscious is made up of contents that have been consciously experienced individually but for one or another reason been forgotten or suppressed into the unconscious, its composition will as such be unique to each individual. The collective unconscious however contains psychic material that is common to mankind and hence universal and impersonal; as such the collective unconscious occupies a deeper psychological level than the personal unconscious.

ARCHETYPES

Archetypes reside in the collective unconsciousness and can be described as mental structures or patterns that influence human behaviors, thoughts and feelings in mirroring expressions. They take many forms but are however a finite number and remains, in its forms, static over time, and can be of a character nature, such as The Great Mother or The Warrior or of a situational nature, such Birth or Death or of an object nature, such as Moon or Fire. Archetypes are universal and timeless and hence appear in all cultures, albeit its manifestations can differ in different settings and time epochs.

Like instincts, archetypes are innate and passed on over generations through the genes, broadly one can distinguish archetypes from instincts in that instincts provides an inherent predisposition towards certain behaviors whereas archetypes provides predispositions towards ideas and zeitgeists although the boundaries are not entirely clear cut and there will be overlaps.

As archetypes are dynamic and autonomous, they take different energy levels; from a dormant state with no transcending impact on human thoughts and ideas to various degrees of active states, where the archetype can be resembled to the invisible force of a magnet that draws humans into predetermined thought patterns. Once the archetype becomes active, it will unconsciously start to impact humans and in time approach the surface, i.e. the conscious, and as such archetypes influence what will be acted out in the financial markets in terms of mood sentiments. Although archetypes provides structure to thought forms and ideas they do not provide the contents, however by reviews and backtests of previous manifestations and actions linked to specific archetypes it is possible to infer notions of the contents.

The reason why specific archetypes activate with various timings, intensities and frequencies is still being debated and explored. One of several explanations is that archetypes represents suppressed instincts and dispositions that have been pushed back into the unconscious from the conscious and to balance the mental composition, the corresponding archetype activates and eventually pushes back into the collective conscious.

SYMBOLS

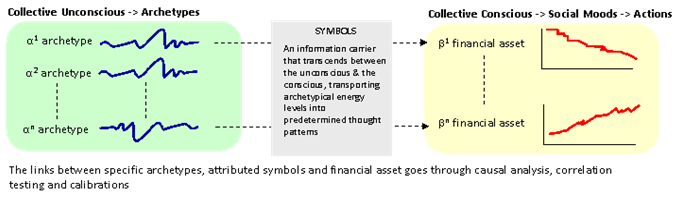

What mechanism do archetypes use to influence the collective behavior with? Symbols, which can be defined as information- and energy-carriers representing different aspects of the many archetypes and the frequency of symbol occurrences provide insights to the activity levels of specific archetypes. Symbols will hence give cues on which archetypal driving forces that will affect social moods. It is important to distinguish symbols from signs in that the symbol contains an unconscious element in addition to its conscious meaning, for instance war word related metaphors or birth related metaphors that occurs in non-war respectively non-birth context can provide insights on the unconscious element of the symbols. Through the study of symbols one can deduct and highlight the fact that people often says/writes one thing and does something entirely different as a representation of an ongoing archetypal transcendation. A sign, on the other hand, contains no unconscious element, i.e. a ’stop sign’ is simply a ’stop sign’ and nothing else.

DEVELOPING A MEASUREMENT METHODOLOGY

As it is not possible to directly observe the collective unconscious, a measurement methodology, with a view to capture archetypical energy movements, can then only be developed to track proxies that represents the archetypal energies. As highlighted, archetypal forces leaves traces in forms of symbols, that can be picked up and measured with regular intervals. By attributing symbols, expressed as words, to the characteristics of the various archetypes, it is possible to, in a composite structure, track the intensity of archetypes and make forecast in terms of social actions, their timings, directions and scales.

Linking symbol as attributes to archetypes

Symbols can be captured using two main conduits; either through dream analysis or through the count of symbols pulled from a broader variety of media sources. Dreams have the disadvantage that they can relate to both the personal as well as the collective unconscious and a clear distinction needs to be made in order to avoid contaminations from the personal unconscious. In addition, to get a consolidated view of the collective unconscious, one would need to collate dreams from an extended and varied test population to be able to draw out the generic collective unconscious dreams.

There will also be issues with defining the dreams objectively and assigning an intensity measure to individual dreams in order to develop time series. So in all, the practical problems with setting up a population of individuals willing to report their dreams on a regular basis and the cleansing and ascertaining of objectivity makes dream reviews a cumbersome and less feasible option.

A more viable option is then to track and study symbols through media sources, but before one can engage in a data pulling exercise, a universe of symbols needs to be defined, categorized and attributed to the full population of archetypes to in a composite manner provide descriptions of the archetypes. As archetypes can be grouped as characters, situations and objects, so need symbols to be selected such as they in a composite way reflect the individual archetypal facets. Symbols related to archetypes thus counts in its hundreds but once they have been mapped to archetypes they generally remained fixed as the archetypal characteristics do not change, although regular screens must be conducted to add newly introduced synonyms to both symbols and archetypes.

Data sources

As the focus is on connecting the energy level of archetypes to globally related financial assets, with a tilt towards the US, the data sources deployed need to cover the larger part of English speaking media worldwide. Also, given the collective unconscious universal and all encompassing nature, data pulling points should not only be within sections of financial and political broadcasts but cover all types of news including culture and sports as expressions of archetypal symbols will occur in all different genre and media. The more dispersed media areas symbols can be drawn from, the higher the likelihood that they represent the collective unconscious rather than various individual’s personal conscious.

Capturing and cleansing

The capturing of symbols is based on a daily word count from the selected data sources. Symbol words needs to be adjusted, filtered and removed to distinguish between words that have with multiple meanings, i.e. they can both be a descriptive word or a noun versus the name of a person or brand/firm product, examples would be Moon or Apple. The filter- and cleansing process hence requires investigations at the most atomic level, i.e. article-by-article, although rudimentary semantic rules and algorithms can be established as an initial filter.

An algorithm to assign different weightings to individual articles or images containing symbol words based on the number of viewings is also required to gauge the relevance between different symbols. Finally, the influence the archetype has on the collective conscious needs to be represented as a normative taxation versus the total flow of information, hence the symbol count is put in context of total number of articles published for the corresponding time duration.

Statistical testing – financial indexes versus times series of symbols

Once daily time series of the symbol counts been cleansed and generated, they can be tested one-by-one for leading correlation versus time series of financial assets. However if correlation is found it is generally of a partial nature, given the nature of archetypes’ activities in that they only indicate large movements in normally one direction, rarely both. This puts constraints on what statistical test methods one can deploy, as R-square values comparing two time series with such different characteristics seldom will be very high.

Also, the archetypes character can be described in a binary status, i.e. either as ‘slumbering’ versus intense spurts of activities that point toward a significant move in the corresponding financial asset. Depicted in the chart below, the archetype generally ‘slumber’ within a tight range without influence on the matching financial instruments and then in a irregular and sporadic manner becomes active and triggers an impact on the price performance of the financial asset. Only through a visual inspection can one establish what the individual slumber lines and trigger points for each symbol are.

With regards to selecting financial assets, our current focus has been on assets with a global magnitude, primarily traded in the US, including;

- S&P500

- VIX

- Gold

- Oil

- DJUSDN – Dow Jones US Defense Industry Index

- DJUSCA – Dow Jones US Gambling Index

Focus is on broader indexes rather than individual stocks as they corresponds better to the general market view and filters out any specific company related idiosyncratic news. The time duration for the tests has generally been the last 8-10 years as that well represents a shift toward a more globalized approach in terms on investing, where access to markets has been made more readily available than previous decades.

Establishing composite archetypes indexes

Establishing leading and partial correlation between symbol time series and financial indexes is one thing, determine causality is quite another. In-depth knowledge about the attributes of the archetypes is pivotal as that will provide guidance to which financial asset they might or might not have either a positive leading correlation or a negative leading correlation. An archetype generally can be attributed more than one symbol so another way of determining causality is to identify whether symbols linked to a particular archetype are activated at the same time, this of course increases the likelihood for causality. To facilitate this work, a mapping table between archetypes and symbols needs to be established. If only some of the mapped symbols correlate, one can generally conclude that the hypothesis of an activated archetype is false.

Clustering symbols with individual weighting will form an econometric equation that expresses a composite index that tracks the activity of the particular archetype. To accommodate the testing, corresponding or opposite symbols can be used to verify or reject causality for the particular symbol.

Backtesting and calibration

To ensure validity in pre-cursor symbol signals, recurring backtesting needs to be conducted of the symbol components in the archetype composite indexes, to confirm that the leading partial correlations holds true over time. In addition to running statistical tests of the correlating time series, tests using contrasting symbol words versus the financial times series are also performed to look for the expected negative correlation.

Also, we are only incorporating archetypes that have been activated several times over a multi-year period to have enough occurrences to ensure validity in the statistical tests and reduce the likelihood of correlation due to pure randomness given the scarcity of ‘testable’ events.

Calibration also links to word analysis, to ensure removal of multiple meaning words as well as additions, as necessary, in terms of new archetype- and symbol synonyms.

OTHER AREAS & RESEARCH IN PROGRESS

The collective unconscious and archetypes influences of course more areas than the financial markets given its all-encompassing extended impact on social mood and actions, including consumer choices, advertising, political preferences and even decisions to start uprisings or go to war. However as our prime focus is on archetypical influences on the financial markets, we will mainly continue to explore additional archetypes that can provide strong forecasting capabilities on financial assets as well as continue to backtest and calibrate existing ones, other fields will be touched upon only if they might have a bearing on the pricing of financial assets. We are also looking into the archetypal impact to other financially related areas such as risk measurements including Value-at-Risk (VaR) and stress tests in market risk and Probability of Default models as part of credit risk measurement.

The focus of our current archetype composite indexes has mainly been to link to financial assets of a global stature and our symbol measurements confined to English speaking media, as a next step we are looking to identify culturally localized archetypes to Chinese language symbols and test them against local Chinese financial assets where the global influence is minor.

What regards to the nature of the archetypes themselves, there are still several open queries we are researching, among others;

- Why do archetypes activate and is it possible to foresee a dormant archetype becoming active? Also, can several archetypes be active in parallel, with different strengths and with different lead times? What are the different time spans that archetypes activate within?

- If one is able to understand why archetypes activate, is it then thus possible through subliminal stimulation to impact its energy level, or is the fact that they belong to the unconscious make conscious influence per definition impossible?

- Is it possible to define constants between archetypal activities and its corresponding reflections in the financial markets, i.e. constants in terms of time lags, duration and intensity?

- How exactly does the symbol signal transfer and subsequent mood formation evolve? Is it possible to identify the portents of the archetypes and symbols, who are they? Why, when, how and where? Can one model how symbols spread using memetics or a tipping point approach? If possible, can then pre-cursors of pre-cursors be developed?

REFERENCES

John Bollen, Huina Mao, Xiao-Jun Zeng – “Twitter mood predicts the stock market”, Journal of Computational Science 2 (2011) 1-8

Ben Graham – The Intelligent Investor

Alan Greenspan – “The Challenge of Central Banking in a Democratic Society”, 1996-12-05

Carl Gustaf Jung – Collective Works

John Maynard Keynes – The General Theory of Employment, Interest and Money

Robert R Prechter & Wayne D Parker – The Financial/Economic Dichotomy in Social Behavioral Dynamics: The Socionomic Perspective